10.19.23

Indiana Multifamily Market Update Through Q3 2023

In any cycle, a buzzword often takes the forefront in discussions and valuations, and it may be surprising, but today, it’s “expectations.” While many believe that interest rates and their unprecedented hikes should dominate the conversation, they are just one piece of the puzzle.

In this report, Advisor Kyle Sissell and associate Noah Shutan delve into the multifamily landscape in Indiana, with a focus on the events, metrics, and trends throughout Q3 of 2023. From client discussions to debt markets and the evolving rental sector, their aim is to offer a concise overview of the multifamily market in the state.

Convos on Capital Markets – Kyle

This may not be new information, but the impact of rising interest rates on the multifamily sector is becoming increasingly evident. The situation is compounded by the nation’s surging economic growth, as indicated by the latest reports. While these may appear to be lagging indicators, there is a widespread expectation of continued rate increases, which further hampers deal flow.

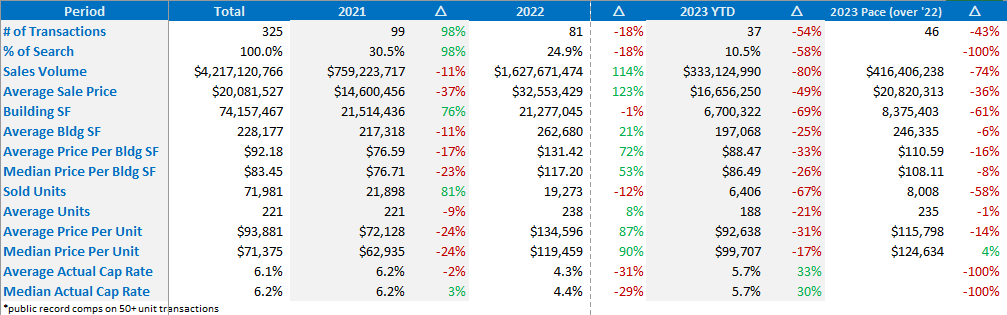

Another factor at play is that sellers’ expectations are still anchored in the past, particularly in terms of pandemic-era pricing. Meanwhile, buyers are actively scouring the market for properties aligned with today’s market realities. In short, the pricing gap still persists. This is starkly evident in a graphic presented later in the article, which projects a 74% drop in deal flow from 2022 to 2023 in the state of Indiana.

To provide better guidance to our clients, we have made several adjustments to our internal valuation methods over the past twelve months. Much of this was informed by discussions with leading appraisers and lenders. One recurring theme has been the necessity to consider properties that were traded prior to 2023 as obsolete sale comps due to the evolving conditions in debt markets.

The debt service coverage ratio has presented a challenge for many of our valuations, resulting in loan-to-value ratios (LTVs) ranging from 50% to 60% for new debt. Understandably, this has not generated sufficient interest from buyers in the value-add space to make offers that are worth considering. Even with assumable debt, we have observed an average LTV of around 62% on properties our team has reviewed.

The situation is further complicated by the 10-year treasury yield, which is hovering around 4.6% this week. All macroeconomic indicators are pointing towards another Federal Reserve interest rate hike by year’s end. In anticipation of this, our clients who are planning to refinance in the coming months have rekindled their relationships with local and regional banks. These banks often offer lower debt service coverage ratio (DSCR) requirements, higher leverage, and greater flexibility for borrowers compared to agency debt. While bank rates may be slightly higher, clients are positioning themselves for an exit or recapitalization when the treasury yields come back down.

Rent Trends – Noah

Discussions with property owners in Indiana highlight a common theme: slowing rental growth. This is a by-product of both an expensive economy and owners stalling their rental increases to hedge against vacancy. In select submarkets, owners are expecting expense growth to negate and even outpace rental growth over the next 12 to 24 months.

Above all, the common theme in Indiana remains true: slow and steady.

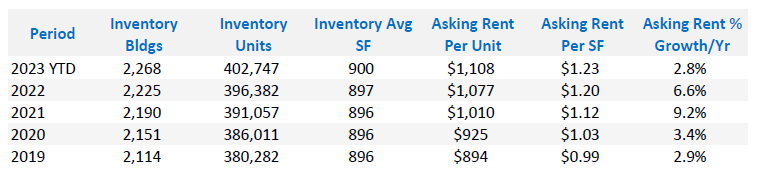

Here’s a look at the rental trends in the state of Indiana over the past five years:

The average overall market rent in Indiana is settling around $1,108 in Q3 2023, marking a substantial slowdown but continued growth of 2.8% year-over-year.

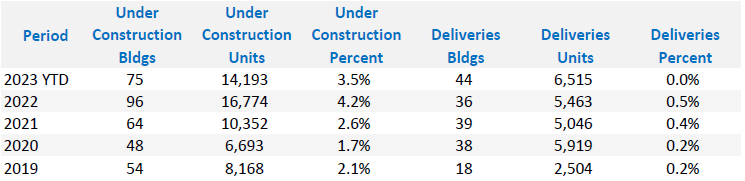

Additionally, Indiana has nearly 14,193 units under construction, which is 3.5% of the current stock – a less than concerning number in comparison to the number of units coming online in the smile states. Overall, Indiana has sustainably offered new housing as outlined in the graphic below.

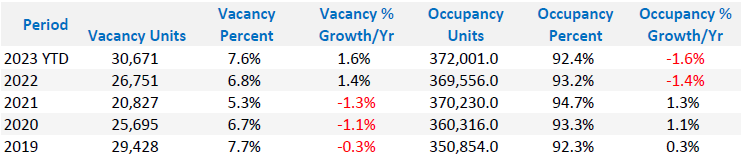

Occupancy in Indiana – Kyle

Factors like remote work opportunities and a thriving job market tied to industries like manufacturing, medical, energy, education and warehousing have contributed to strong occupancy and renter interest across the state. The continued frenzy for single-family home prices and elevated home interest rates has further aided multifamily owners. Below provides a state-wide snapshot of occupancy over the past five years in the state.

Market Dynamics – Noah

Out-of-state operators have recognized Indiana’s potential, contributing to the rise in top-of-market prices. The Midwest’s durability and potential for value-add property cycles have made it an attractive investment destination.

The graphic below highlights filtered sales data over the past five years for your typical sub-institutional ‘value-add’ property, covering 50+ units and built prior to 1990.

Again, no surprise that expectations and debt have played an integral role in slowing down deal flow across the state. One interesting point is that if the estimated pace holds, we’ve only reset to early-pandemic averages.

Predictions for the Market – Kyle & Noah

Despite the challenges in capital markets, Indiana’s multifamily market is poised for continued growth. Limited inventory has led to off-market offers and record-setting prices in submarkets. Additionally, the state has consistently advocated for the evolution of its job market through both public and private investments and pro-business initiatives, benefiting renters and property owners alike.

With balanced market dynamics in place, fluctuations may occur, but Indiana is anticipated to maintain healthy, stable, and long-term growth. This growth is driven by robust demand for value-add properties and competition from a range of investor types, including local investors, existing property owners, and new out-of-state players.

While deal volume is likely to remain low in the coming year, we anticipate that by Q4 of 2024, we will begin to see a return to the equilibrium experienced in the pre- and early-pandemic years.

How Can We Help?

If you need assistance in assessing the value of your property or require proprietary market information and data, please feel free to reach out. You can also connect with us on LinkedIn for the latest updates and insights.

https://www.linkedin.com/in/kylesissell/

https://www.linkedin.com/in/noah-shutan/